Millennials and Life Insurance

Millennials and Life Insurance

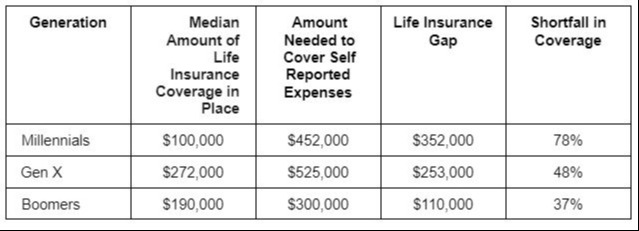

Sorry, not sorry, Millennials about some important facts related to your generation. While Millennials (born between 1981-1996) generally tend to be better educated and more tech-savvy than Gen X (born 1965-1980) and Boomers (1955-1964), they also tend to leave their families less financially secure or in debt upon their untimely demise. According to a recent “Life Insurance Gap”1 survey conducted by New York Life Insurance Company, Millennials are the generation most at risk for financial hardship due to inadequate life insurance coverage. The survey asked Americans to compare how much life insurance they thought they needed to protect their loved ones and meet their financial obligations versus the amount they have in place.

The table below shows the shortfall for each generation and the numbers are troubling:

Similarly, The Atlantic found that “while the share of Americans covered by life insurance slid from 63 percent in 2011 to 52 percent in 2021, and is 48 percent as of Sept 2023, the shortfall is most pronounced among people under 40.”2 This correlates with another surprising trend, Millennials are also less healthy than their older counterparts. Based on a recent Blue Cross and Blue Shield Health of America report, “Millennials begin to see a higher prevalence of physical disorders driven by cardiovascular and endocrine conditions (eg. diabetes), making them unhealthier than their Generation X counterparts.”3 Another study by Blue Cross and Blue Shield estimates that without intervention, Millennials could see mortality rates increase to 40% more than Gen-Zers of the same age.

Why Millennials Should Buy Insurance NOW:

Despite the seemingly bleak statistics, Millennials have several advantages over Gen-X and Boomers --

1) Cost Savings. While things like cell phones, streaming services or the vast majority of things cost the same for all generations, insurance is not one of them. Life insurance is considerably less expensive when we’re younger. To illustrate, $1 Million of life insurance protection for a healthy male Age 30 is roughly 30% cheaper than the same policy for a 40-year-old.

2) Insurability. For the general Millennial population, health is rapidly deteriorating. Purchasing insurance when younger and healthier protects insurability or the ability to get coverage before the onset of health issues that arise as we age.

3) Debt. Millennials carry more debt than prior generations at the same age. For Millennials who are married, have children or own a home, the consequences to the family who don’t have the financial resources upon death are obvious and devastating. For others who haven’t started a family, many have student loan debt that was co-signed by a parent or grandparent which is still an obligation that must be repaid by the co-signor.

4) Job-Hopping. Millennials tend to change jobs or careers much more frequently than Gen-X or Boomers and with each job change, they lose their insurance coverage, including life insurance. Purchasing individual coverage ensures they will still have life insurance regardless of job changes, layoffs, terminations, or changes to health.

The Good News:

In this technology age, it’s much simpler and easier to buy insurance than ever before. And as mentioned above, much cheaper for applicants who are younger and healthier. For less than the average Doordash bill, Millennials can protect their families, their insurability for the future and give themselves some peace-of-mind.

1 New York Life Insurance Company, Life Insurance Gap. November, 2018.

2 Michael Waters, The Atlantic, Millennials, What Will It Take For You To Buy Life Insurance? July, 2021.

3 Blue Cross Blue Shield, The Economic Consequences of Millennial Health. November, 2019.